Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

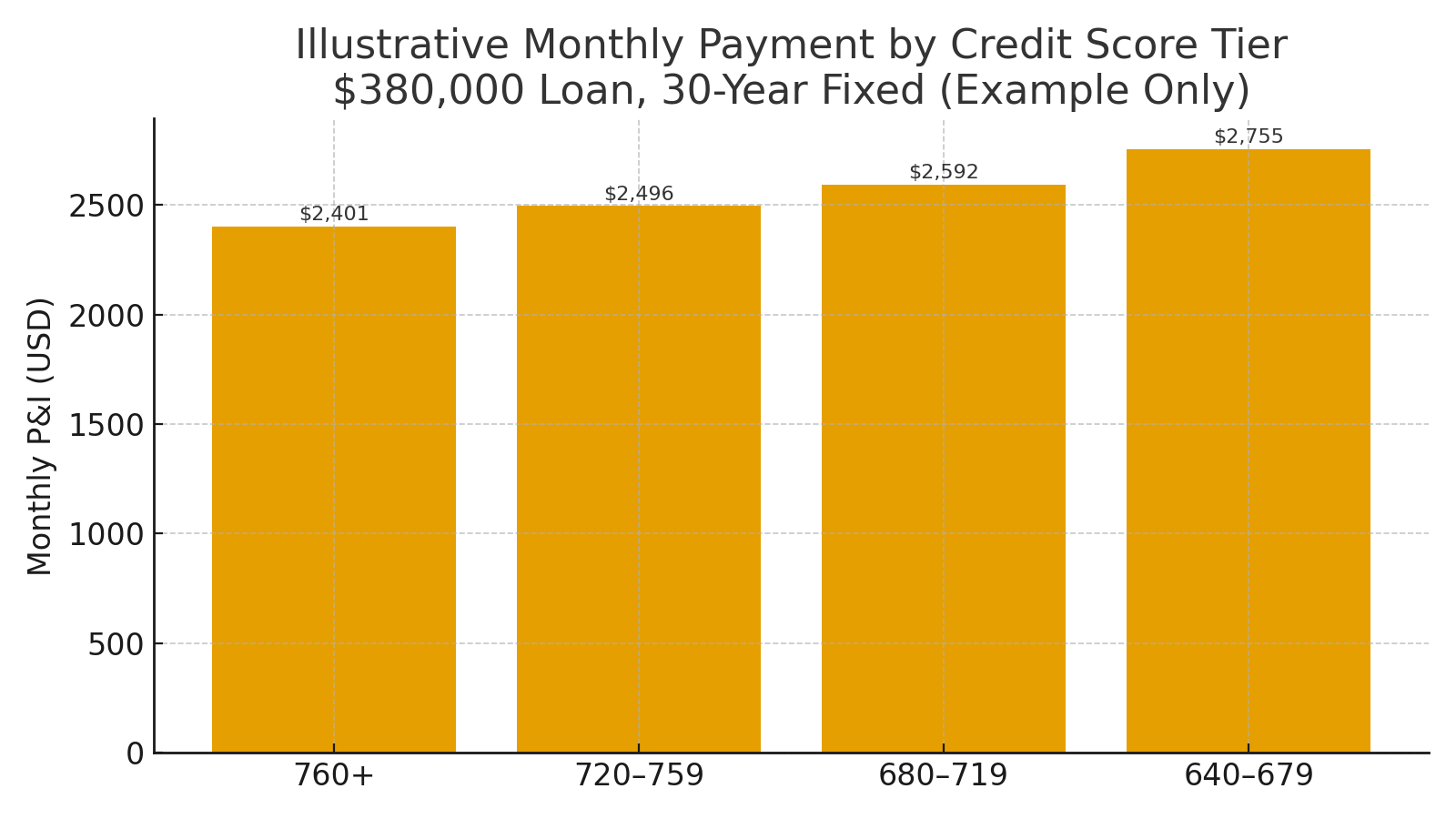

Your credit score affects both approval and pricing; therefore, understanding where you stand—and how to improve—can meaningfully lower your monthly payment. Even a 20-point difference may place you in a better pricing tier, which can translate into real savings.

First, check your reports. Because your score is built from the data in your credit files, start by pulling your free reports and reviewing them for accuracy. If you find errors, dispute them promptly so negative items don’t work against you.

Next, focus on high-impact moves. Generally, these practical steps deliver the most improvement in the shortest time:

-

Lower utilization: Pay revolving balances below 30%—ideally under 10%—of limits.

-

Protect payment history: Set autopay or reminders; since payment history weighs most, on-time streaks matter.

-

Avoid new debt: Meanwhile, hold off on opening new accounts or financing big purchases.

-

Tidy up errors: Furthermore, remove inaccurate late payments or duplicate collections through proper disputes.

Then, get credit-aware pre-approval. With that in mind, a local lender can review your file and suggest targeted tweaks before you write offers. In many cases, a small score bump can improve your interest rate, which in turn reduces your monthly payment (see the illustrative chart above).

Finally, match loan programs to your profile. Although conventional loans tend to reward higher scores with better pricing, FHA may offer more flexibility if your score or DTI is still improving. Consequently, comparing options side-by-side helps you choose the best path.

Bottom line: Ultimately, a cleaner, stronger credit profile means better terms, smoother underwriting, and more confidence when you make an offer.

Talk to a Trusted Lender

I’ll introduce you to a local lender who can review your credit, share exact score tiers, and outline quick wins—no obligation.

Prefer text? Text “LENDER INTRO” to 774-289-7552.