Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Saving for a down payment can feel daunting; however, most first-time buyers don’t need 20%. In many cases, 3–5% down is enough, and certain programs allow even less (or none for eligible VA/USDA buyers). To plan effectively, break your cash needs into three buckets: down payment, closing costs, and prepaids/escrows (the setup for property taxes and insurance).

First, understand the typical ranges. Generally, conventional loans start at 3–5% down, while FHA is often 3.5%. Meanwhile, closing costs commonly add several percent to your total, including lender fees, title/settlement, recording, and prepaids. Therefore, your “cash to close” is usually higher than the down payment alone.

Next, explore ways to reduce cash to close. For example, you can negotiate seller credits to offset some closing costs, or select lender credits (a slightly higher rate in exchange for lower upfront costs). Additionally, properly documented gift funds from immediate family are common. For Massachusetts buyers, consider MassHousing and the ONE Mortgage program, which may offer down payment assistance or reduced mortgage insurance for eligible borrowers.

Then, weigh the tradeoffs. Although a 20% down payment removes PMI and lowers the monthly cost, waiting to reach 20% isn’t always necessary. If rising prices or rents are outpacing your savings, buying sooner with a smaller down payment—while preserving an emergency fund—can still be the smarter path.

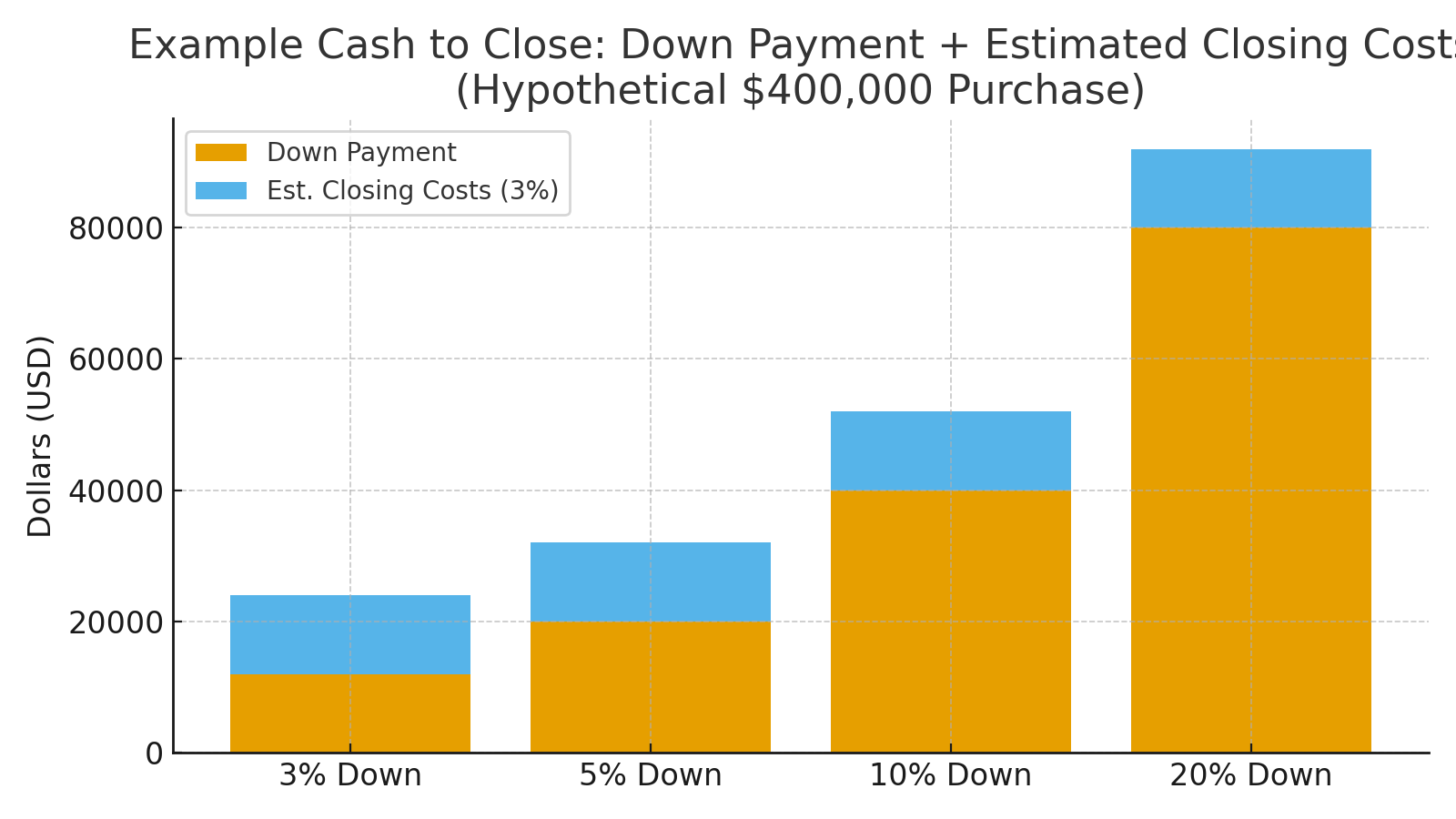

After that, compare scenarios side by side. With that in mind, look at 3%, 5%, 10%, and 20% options and note the differences in monthly payment, PMI, and cash to close. (See the illustrative chart above for how cash needs scale.) Ultimately, the “right” down payment balances comfort, approval, and timeline—so you can shop with confidence.

Finally, get specific with your towns. Because taxes, insurance, and condo/HOA fees vary by location, your numbers can change from one town to the next. Consequently, a quick, tailored estimate helps prevent surprises.

Ready to explore your loan options?

I’ll introduce you to a trusted local lender to review down payment choices, credits, and monthly payment—no obligation.

Prefer text? Text “LENDER INTRO” to 774-289-7552.