If you’re buying your first home, “How much can I afford?” is the right first question. To begin, start with a monthly payment you feel comfortable making—then work backward to the purchase price.

First, clarify your monthly budget.

List your fixed expenses—car, student loans, minimum credit cards, and subscriptions. Next, add a cushion for savings and emergencies. After that, whatever remains is the safe amount you can devote to housing. Importantly, choose a number you can live with during slower months, not just your best month.

Meanwhile, understand DTI (debt-to-income).

Lenders compare your gross monthly income to monthly debts. Generally, most programs have target ranges, and, as a result, strong credit, stable income, and conservative debts improve approvals. However, your lender’s maximum isn’t always your comfort zone—so, use the lower of the two.

Outbound resource: Learn how DTI works at the CFPB (Consumer Financial Protection Bureau): https://www.consumerfinance.gov/ask-cfpb/

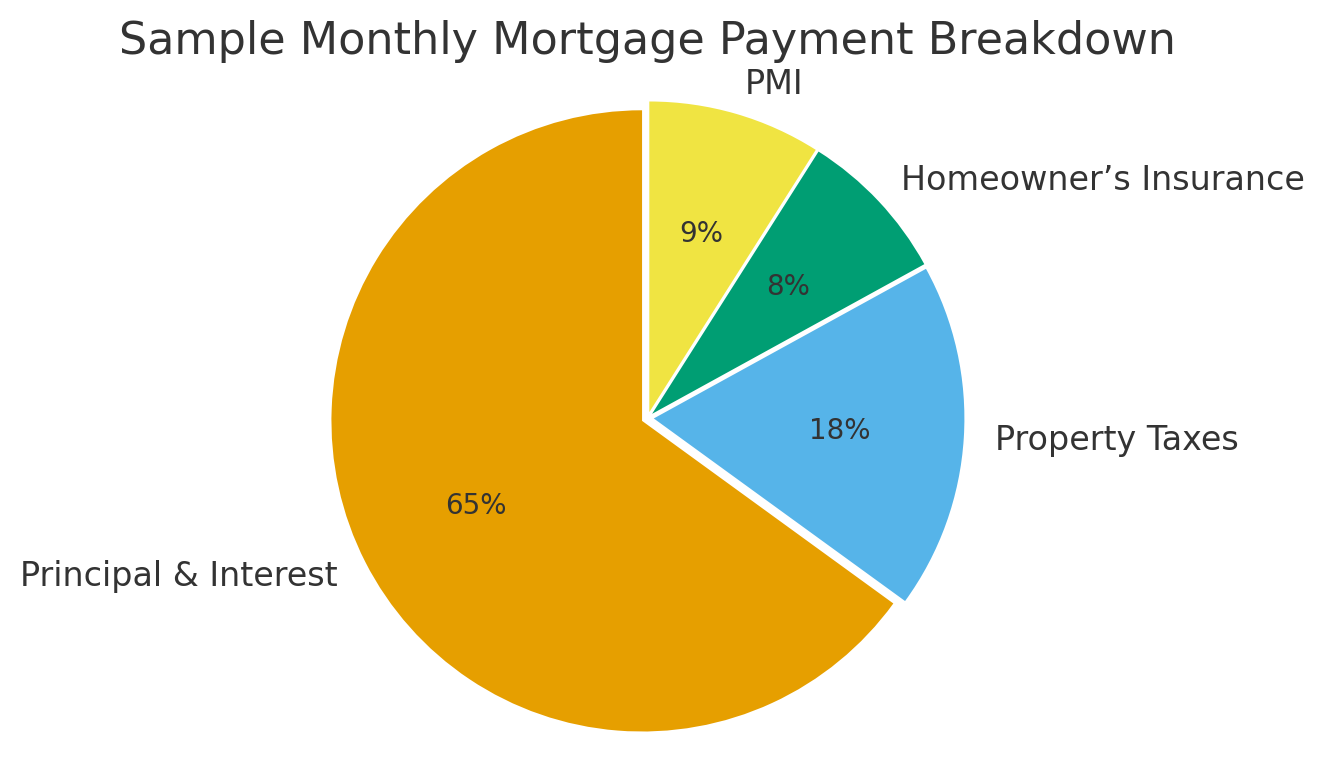

Now, break down a mortgage payment.

Your payment usually includes principal and interest, property taxes, and homeowner’s insurance; in addition, you may see HOA/condo fees and mortgage insurance (PMI). Because Massachusetts property taxes vary by town, budget with the towns you’re actively targeting. For example, two similarly priced homes in different towns can produce different totals.

Outbound resource: Read a plain-English PMI overview at the CFPB: https://www.consumerfinance.gov/ask-cfpb/

Then, plan for cash needs and reserves.

Even with low down payment options, you’ll still have closing costs. Moreover, you should keep a reserve for maintenance and unexpected repairs. Consequently, a slightly lower purchase price that preserves your emergency fund can be the smarter choice.

Outbound resource (MA): Explore MassHousing programs: https://www.masshousing.com/

Consider rate and price scenarios.

Payments shift when rates move—therefore, it’s wise to model three options: conservative, target, and stretch. With that in mind, we’ll run side-by-side estimates so you can see how a small price or rate change affects your monthly payment and cash to close.

Outbound resource: Try a reputable mortgage calculator (e.g., Fannie Mae or Freddie Mac).

Finally, align the numbers with your lifestyle.

Commuting costs, childcare, and hobbies all affect what truly feels affordable. Ultimately, the best budget is the one that supports your whole life, not just your mortgage.

Want a custom affordability plan for your preferred towns? I’ll run numbers and options side-by-side.